")

")

")

")

")

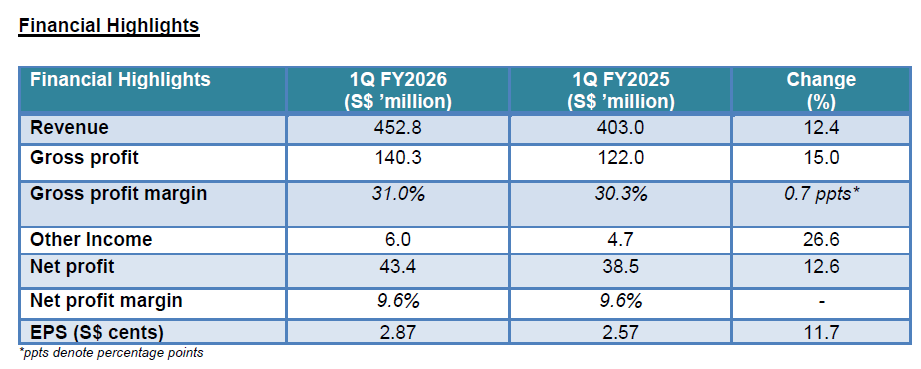

- Revenue increased to S$452.8 million, mainly supported by contributions from new store openings since FY2025 and festive sales for Lunar New Year and Hari Raya Puasa.

- Gross profit increased 15.0% to S$140.3 million with an improvement in sales mix and to combat rising business costs.

- 3 new stores were secured, with 2 targeted to open in 2Q FY2026 and 1 in 3Q FY2026.

Singapore, 29 April 2026– Sheng Siong Group Ltd. (“Sheng Siong”, together with its subsidiaries, the “Group” or “昇菘集团”), one of the largest supermarket chains in Singapore, reported a net profit of S$43.4 million for three months (“1Q FY2026”) ended 31 March 2026, an increase of 12.6% year-on-year (“yoy”).

Revenue for 1Q FY2026 increased by 12.4% yoy to S$452.8 million, up from S$403.0 million in the same period last year. The increase was mainly driven by contributions from 12 new store openings in FY2025, as well as festive sales during Lunar New Year in February and Hari Raya Puasa in March. Gross profit grew by 15.0% yoy to S$140.3 million in 1Q FY2026, while gross profit margin improved by 0.7 percentage points yoy to 31.0%, supported by continued enhancements in our sales mix, which helped offset higher operating costs.

Other income increased by 26.6% yoy to S$6.0 million in 1Q FY2026 as compared to 1Q FY2025. The growth was mainly driven by higher government grants received from the enhanced Progressive Wage Credit Scheme (“PWCS”) during 1Q FY2026, a reduction in net exchange losses yoy, and an increase in miscellaneous income.

In 1Q FY2026, the Group’s operating cost increased due to a 12.8% yoy increase in administrative expenses to S$17.8 million and a 15.6% increase in selling and distribution expenses to S$76.1 million. These were mainly due to higher staff cost due to higher headcount to support more stores and higher variable bonuses driven by better financial performance, as well as higher depreciation arising from the additional leases of supermarket stores and land lease of Sungei Kadut, for the Group’s new Distribution Centre. Cash flow from operating activities in 1Q FY2026 increased by S$11.6 million compared to the same period last year, mainly due to higher profit and more non-cash/digital payments received during the current quarter. As of 31 March 2026, the Group’s cash and cash equivalents balance increased by 5.9% yoy to S$461.1 million from S$435.5 million as at 31 December 2025.

Looking Forward

Geopolitical tensions, particularly the conflicts in the Middle East, continue to pose macroeconomic uncertainties and energy risks. The Ministry of Trade and Industry (“MTI”) has revised the country’s GDP growth forecast to 2.0%–4.0%[1], while the Monetary Authority of Singapore (“MAS”) expects core inflation to rise to 1.5%–2.5%, up from an earlier forecast of 1.0%–2.0% previously[2]. The sharp increase in energy costs, along with potential spillover effects to the prices of related goods and services, may lead to increased operating costs. Furthermore, supply chain disruptions may also arise from geopolitical rivalries, such as the ongoing war in Ukraine.

These developments present downside risks to the global economy and have made consumers more cautious in their spending decisions. With growing uncertainty around prices and income stability, many households are becoming more price-sensitive and shifting their focus toward essential items that offer greater value. Aligned with this sentiment, the Singapore government has continued to roll out support measures such as the CDC vouchers, which aim to help households cope with the rising cost of living and provide targeted relief for daily essentials.

Against this backdrop, we believe Sheng Siong’s strong value-for-money proposition, supported by competitively priced goods and house brand offerings, positions us well to meet evolving consumer needs, especially as more households seek quality essentials at affordable prices.

To navigate the current uncertain environment, the Group is actively refining its sales mix and focusing on building its core competencies. At the same time, we continue to diversify our supplier base to enhance supply chain resilience, while investing in automation to improve operational efficiency and mitigate rising labour costs.

Mr Lim Hock Chee, the Group’s Chief Executive Officer, said, “The Group remained resilient amid macroeconomic uncertainties and delivered steady performance in the first quarter, reflecting our operational strength and solid fundamentals. Through our prudent cost management and ongoing efforts to optimise our sales mix, we remain dedicated to combating rising business costs, such as increased operational or compliance costs as we increase our store network and develop the new distribution centre.

Looking ahead, we also maintain a disciplined approach to growth, focusing our expansion in areas where we have limited presence. We have secured two new stores at Blk 336 Smith Street, and Blk 120 Canberra Crescent, both of which are targeted to open in 2Q FY2026, and another one at 11 Rivervale Crescent expected to open in 3Q FY2026. In addition, we are awaiting 5 tender results to be released by HDB. Despite the external challenges, we remain confident in our ability to grow and strengthen our presence in the years ahead.”

– End –

[1] https://www.mti.gov.sg/newsroom/mti-upgrades-2026-gdp-growth-forecast-to–2-0-to-4-0-per-cent-/

[2] https://www.mas.gov.sg/news/monetary-policy-statements/2026/mas-monetary-policy-statement-14apr26

{kind=link}